In short: Meta has committed an additional $21 billion to CoreWeave for dedicated AI cloud capacity running from 2027 through December 2032, bringing the total value of the two companies’ infrastructure relationship to approximately $35 billion. The new contract will deliver early deployments of Nvidia’s Vera Rubin platform across multiple sites, and is designed specifically for inference workloads rather than training. Alongside the announcement, CoreWeave disclosed plans to raise $4.25 billion in new debt ,$3 billion in convertible notes and $1.25 billion in junk bonds, to fund continued expansion. CoreWeave shares rose around 5% on the news; Meta shares gained roughly 3%.

From Ethereum mining to a $35 billion Meta relationship

CoreWeave was founded in 2017 in New Jersey as Atlantic Crypto, a commodity traders’ side project mining Ethereum using graphics processing units. When the 2018 cryptocurrency crash made mining uneconomical and Ethereum’s eventual move to proof-of-stake threatened to render GPU mining obsolete entirely, the founders, Michael Intrator, Brian Venturo, and Brannin McBee, recognised that the GPU inventory they had accumulated was also exactly what machine learning researchers needed and could not easily access through conventional cloud providers. The company was renamed CoreWeave in 2019 and pivoted to GPU cloud infrastructure. It went public on March 28, 2025, at $40 per share, valuing it at $23 billion. Its 2025 revenue reached $5.13 billion, up 168% year on year, and its contracted backlog is estimated at more than $66 billion. The first Meta agreement, worth $14.2 billion and announced in September 2025, was the deal that established CoreWeave as a serious counterpart to the hyperscale cloud providers. The April 9, 2026 expansion, an additional $21 billion, makes Meta the most significant commercial relationship in CoreWeave’s history, with a combined commitment that will sustain the company’s revenue base through the end of the decade.

What Meta is actually buying

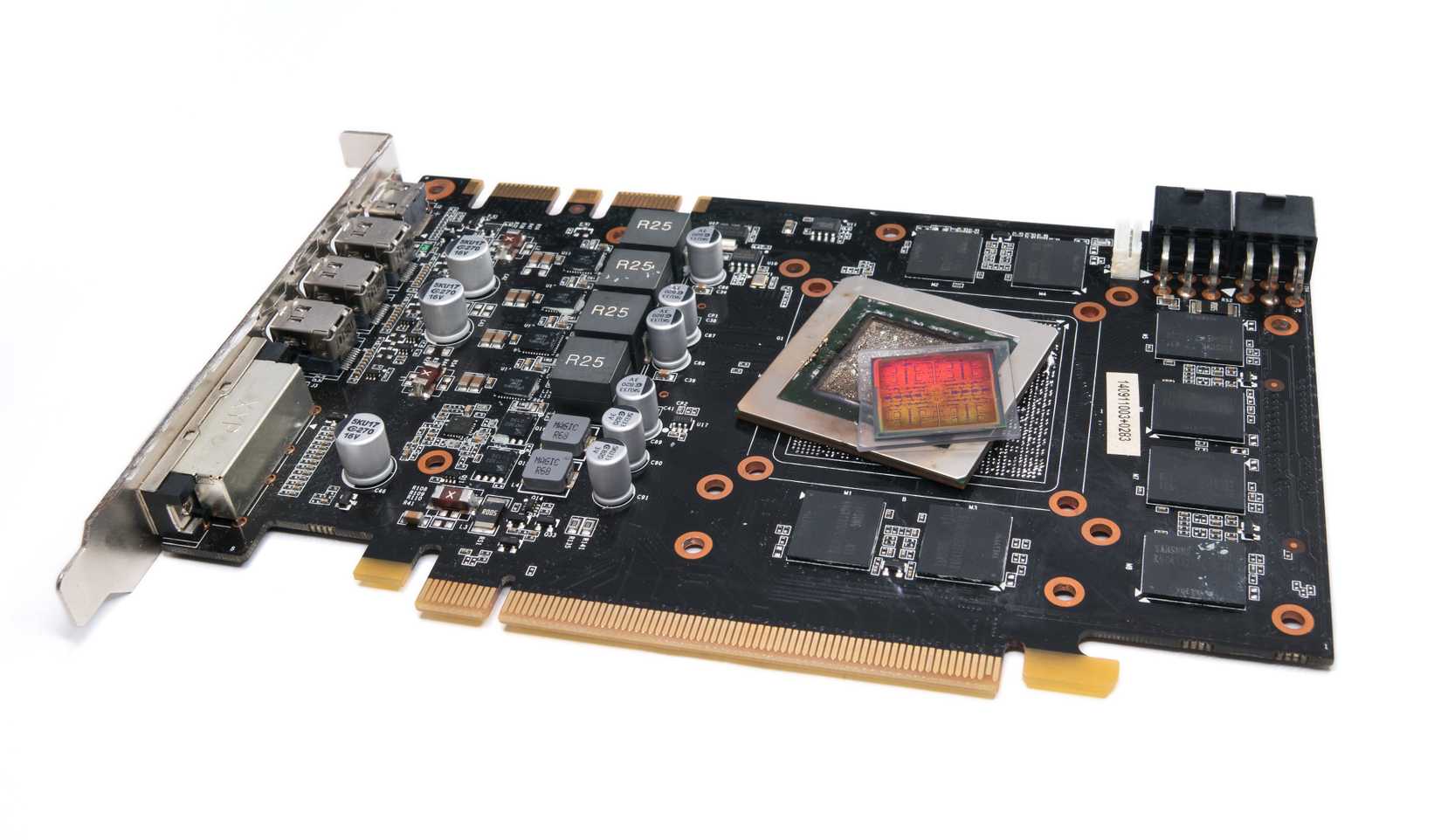

The contract is specifically structured around inference rather than training. Meta’s Llama model family is open-weight and freely downloadable, which means the capital-intensive training phase is largely complete before any cloud contract is signed; the ongoing cost is serving those models to billions of users in real time. Inference at Meta’s scale, hundreds of millions of daily active users across Facebook, Instagram, WhatsApp, and Meta AI, requires sustained, low-latency compute across distributed infrastructure in a way that Meta’s own data centres cannot always absorb at peak capacity. CoreWeave will deploy that capacity across multiple locations and will include some of the first commercial deployments of Nvidia’s Vera Rubin platform, which the chipmaker unveiled at GTC 2026 in March as the next generation of its AI infrastructure hardware. The new deal supplements rather than replaces Meta’s internal build-out. Meta has guided for $115 billion to $135 billion in capital expenditure in 2026, with AI infrastructure identified as the primary driver, and the company has been explicit that it is building both owned data centres and sourcing external capacity simultaneously. The CoreWeave expansion follows a $27 billion infrastructure deal Meta signed with Nebius in March 2026, under which the Dutch neocloud operator will supply dedicated compute starting in early 2027, also featuring early Vera Rubin deployments. The two deals together illustrate that Meta is not simply procuring cloud capacity but building a diversified multi-vendor infrastructure position designed to give it flexibility and redundancy at hyperscale.

The customer diversification play

For CoreWeave, the Meta expansion solves a problem that has shadowed the company since its IPO: excessive revenue concentration. Microsoft represented 62% of CoreWeave’s 2024 revenue, a figure that made institutional investors uncomfortable and that the company has been working to reduce. With the new Meta commitment in place, CoreWeave CEO Michael Intrator said no single customer would represent more than 35% of total sales. That is still a significant concentration, but it is a materially different risk profile from a position where a single hyperscale customer controls the majority of your revenue. Nvidia, which made a $2 billion strategic investment in Nebius in March 2026 and has deepened its commercial relationships with every major AI cloud provider, sits at the centre of CoreWeave’s business model: CoreWeave’s entire infrastructure is built around Nvidia GPUs, and the Vera Rubin deployments in the Meta contract will extend that dependency into the next hardware generation. CoreWeave also recently expanded its agreement with OpenAI by up to $6.5 billion, further broadening its customer base beyond Microsoft. The company’s stock reached an all-time high of $187 in mid-2025 before pulling back to around $65 in late 2025 amid broader concerns about AI investment returns; following the Meta expansion announcement it was trading in the $88 to $95 range.

The debt that funds it all

The 💜 of EU tech

The latest rumblings from the EU tech scene, a story from our wise ol’ founder Boris, and some questionable AI art. It’s free, every week, in your inbox. Sign up now!

AI cloud infrastructure is expensive to build before contracts start generating revenue, and CoreWeave has funded its growth primarily through debt. Alongside the Meta deal announcement, the company disclosed plans to raise $4.25 billion in new financing: $3 billion in convertible senior notes due 2032, carrying a coupon of between 1.5% and 2%, with an option for investors to convert into equity; and $1.25 billion in senior unsecured notes due 2031 at approximately 10%, effectively junk-bond pricing. CoreWeave’s total debt load sits at around $30 billion, roughly triple what it was a year earlier. The company’s argument for the debt structure is that its contracted revenue base, more than $66 billion in backlog, provides sufficient visibility to service the obligations. Intrator has described CoreWeave as an “AI factory” whose capital costs are underwritten by long-term customer commitments before infrastructure is built. The broader AI infrastructure financing environment has been characterised by similarly large-scale debt structures: SoftBank secured a $40 billion bridge loan to fund its $30 billion follow-on OpenAI investment as part of the Stargate project, illustrating that the capital requirements of AI at scale are now large enough to require financing instruments that did not exist in this form even two years ago. The year 2025 cemented AI infrastructure as the primary competitive variable in the technology industry, and CoreWeave, a company that began as a closet of Ethereum mining rigs, has positioned itself as a load-bearing pillar of that infrastructure, one $21 billion commitment at a time.

Stephan is the sports journalist for the Maple Grove Report.