Modern derivatives and digital asset markets operate under a persistent drag of operational friction. A recent Nasdaq survey reveals that 70% of global firms experience settlement failures on a daily basis. This structural inefficiency forces institutions to maintain excess overnight collateral buffers, tying up capital that could otherwise generate returns.

The inability to mobilize assets instantly across disparate systems acts as a constant drain on institutional performance. As market participants look to optimize their balance sheets, tokenized collateral is emerging as a practical mechanism to mitigate these execution frictions. By representing traditional assets on distributed ledgers, firms can reduce counterparty exposure and improve the velocity of their capital across trading venues.

The Counterparty Risk Dilemma in Digital Assets

Traditional cryptocurrency market structures present a fundamental challenge for institutional allocators. Historically, platforms required participants to pre-fund their accounts before executing trades. This model leaves capital sitting idle on trading venues and exposes participants to centralized counterparty risk. TradFi market infrastructure deliberately separates custody and execution as well as clearing to distribute risk. Bringing digital asset markets into alignment with these legacy standards has become a core priority.

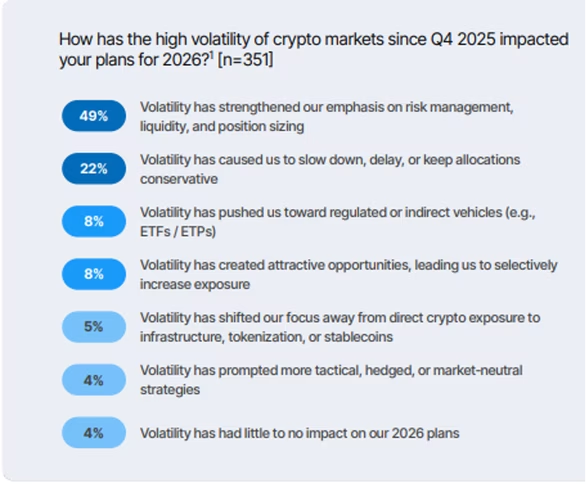

A recent EY-Parthenon institutional investor survey indicates that 49% of respondents have strengthened their emphasis on risk management and liquidity as well as position sizing following recent market volatility. Institutions require frameworks that minimize exposure while maintaining access to deep liquidity.

The 💜 of EU tech

The latest rumblings from the EU tech scene, a story from our wise ol’ founder Boris, and some questionable AI art. It’s free, every week, in your inbox. Sign up now!

Tokenized Money Market Funds as the Yield-Bearing Bridge

Exchanges are adapting their infrastructure to bridge this gap. Catherine Chen, Head of VIP and Institutional at Binance, notes that aligning with traditional standards drives current architectural changes. She explains that “Binance was the very first in the industry to roll out what we call banking tri-party.” By implementing this setup, the exchange aims “to allow the traditional finance type of institutional investor to engage in activity on Binance, but in a way that they’re more used to.” This approach lets participants trade in a familiar environment that “they’re more comfortable with,” effectively decoupling asset storage from trade execution.

The mechanics of this structural adaptation center on off-exchange collateral solutions. Under this model, institutions can pledge yield-bearing assets via a regulated custodian to access trading margin. Participants can utilize tokenized money market fund shares, such as those issued through Franklin Templeton’s Benji platform, keeping the underlying assets securely vaulted with a partner like Ceffu. The custodian then mirrors the asset value for trading purposes on Binance. This completely removes the requirement to transfer the actual assets onto the exchange order book. Institutions can now allocate capital efficiently without compromising their baseline compliance mandates.

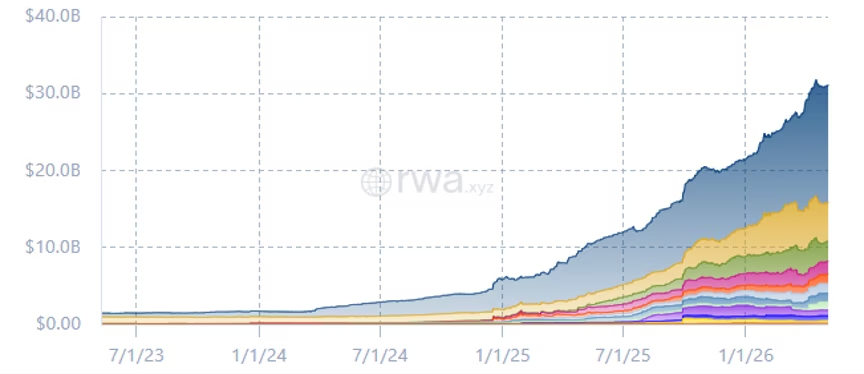

Deploying real-world assets in this manner is gaining measurable traction. Recent data from RWA.xyz shows that total distributed value in this sector has reached $31.12 billion, representing a 45% increase year-to-date.

Moving these assets on-chain addresses specific execution bottlenecks. The same Nasdaq research assessing market friction notes that tokenizing collateral can prevent 1 in 8 failed trades and reduce overall operational costs by 12%.

By deploying tokenized money market funds as trading collateral, Binance and Franklin Templeton provide a system that reflects institutional risk frameworks rather than asking traditional firms to adopt native cryptocurrency settlement patterns.

24/7 Capital Efficiency Meets TradFi Safeguards

The financial benefits of this architecture directly target capital efficiency. Traditional fiat or standard stablecoins deposited on an exchange do not generate yield. They act as a dead weight on a firm’s balance sheet during periods of low trading activity. Tokenized money market funds alter this dynamic. They allow deployed capital to remain fully productive and yield-bearing while simultaneously acting as margin in a continuous 24/7 digital asset market.

This dual utility aligns with a broader shift in how corporate treasuries approach digital assets. According to PwC’s Global Crypto Regulation Report 2026, institutional involvement has now crossed the “point of reversibility.” The consulting firm observes that digital assets are becoming deeply embedded in treasury operations and corporate balance-sheet management, moving far beyond simple speculative trading.

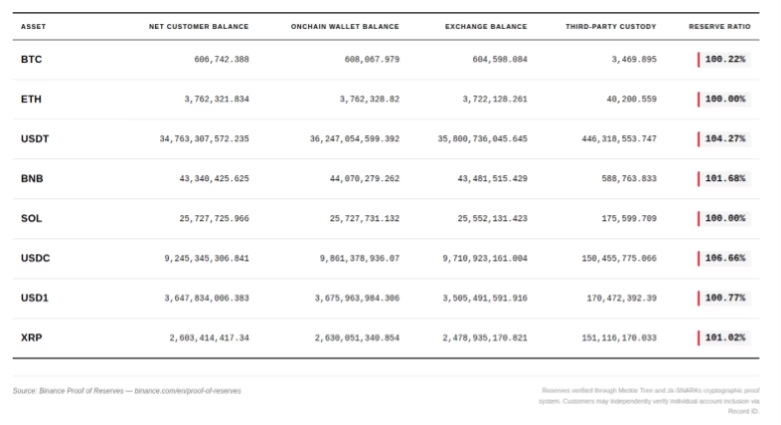

As institutional capital moves deeper into digital asset infrastructure, treasury teams are also demanding higher standards around collateral transparency and reserve verification. Binance, for example, recently disclosed more than $240 billion in net customer assets through its Proof of Reserves system, maintaining reserve ratios above 100% across major assets including BTC, ETH, USDT, and USDC. That type of publicly verifiable reserve reporting is becoming increasingly important for firms evaluating whether digital asset infrastructure can support treasury-scale liquidity management while maintaining institutional risk controls.

Firms are utilizing blockchain rails to move and manage money behind the scenes, integrating these systems directly into their core financial workflows. Off-exchange collateral structures support this integration by maintaining traditional financial safeguards without sacrificing the continuous liquidity of cryptocurrency markets.

An Enhanced Infrastructure for Modern Markets

Utilizing off-exchange collateral and tokenized real-world assets successfully aligns digital asset execution with traditional financial risk standards. Institutions no longer need to accept centralized exchange risk simply to access market liquidity. By holding tokenized shares in regulated custody and mirroring their value for trading, market participants achieve a necessary separation of duties.

It’s an operational upgrade that addresses the capital inefficiencies that have historically penalized firms for maintaining strong risk controls. The digital asset ecosystem continues to mature, and future market resilience will increasingly depend on platforms that can support continuous margin optimization and secure custody architectures.

Stephan is the sports journalist for the Maple Grove Report.