Apple shares closed above $300 for the first time after investors rewarded the company’s stronger-than-expected earnings, surging Services revenue, and massive $100 billion buyback despite continued criticism of its delayed AI rollout.

Apple shares closed at a new record high of $300.23 on May 15, surpassing both the $300 mark and the company’s previous closing record of $287.51 set on May 6. Earlier in 2026, investors worried about delayed Siri features, slowing hardware growth, tariff exposure, and growing competition in generative AI.

Apple stock briefly reached a 52 week high during the trading day of $303.20.

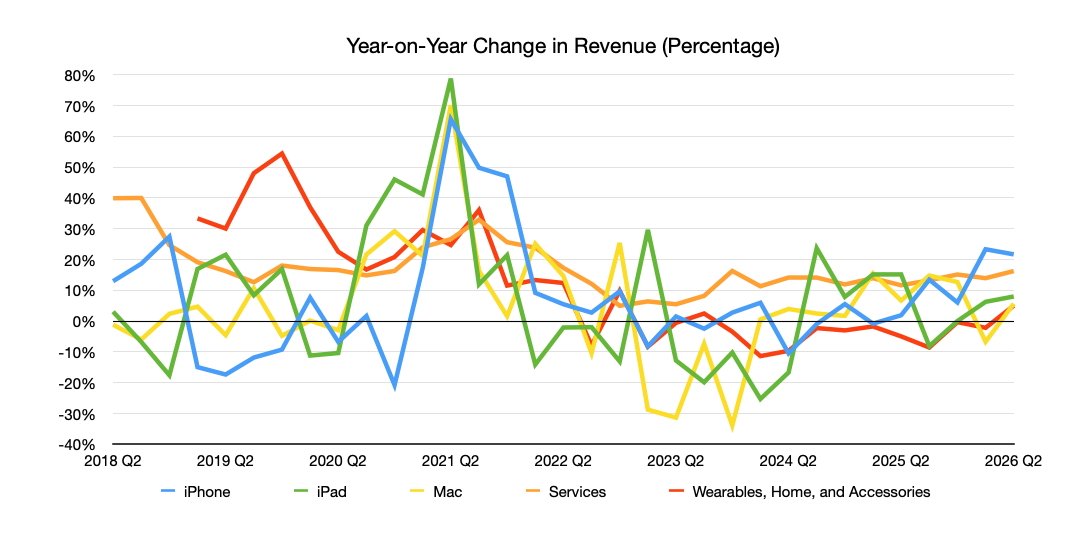

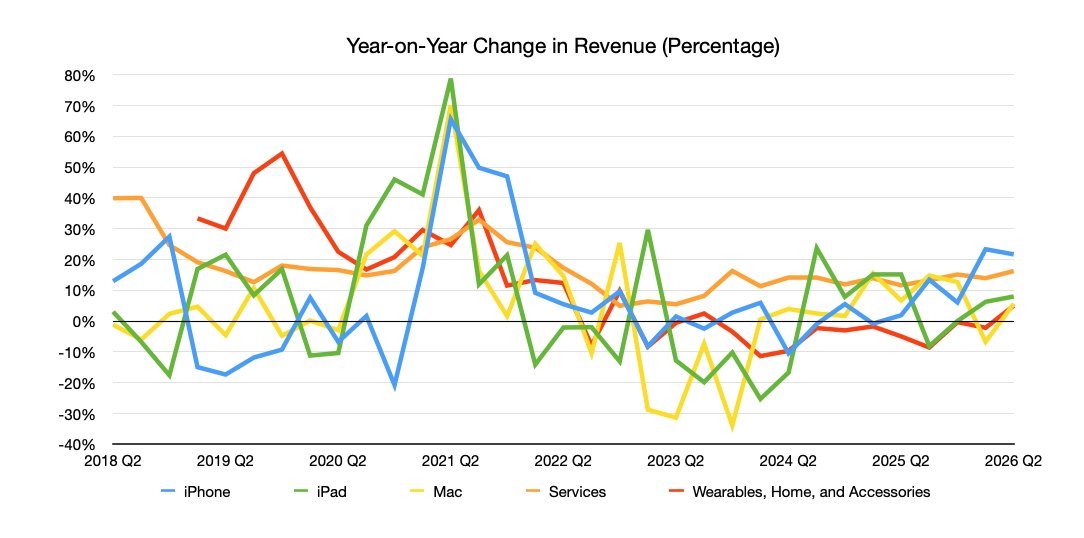

The rally accelerated after Apple reported $111.2 billion in revenue and earnings per share of $2.01 for the quarter ending March 28, both above Wall Street expectations. The company also approved another $100 billion stock buyback and raised its quarterly dividend to $0.27 per share.

Apple generated more than $28 billion in operating cash flow during the quarter, reinforcing investor confidence in the company’s core business. Tim Cook said demand for iPhone remained strong during the March quarter, while Services revenue reached another all-time high.

Greater China revenue jumped roughly 28% year over year after several weaker quarters. The rebound helped calm investor concerns that Apple was losing ground in one of its largest markets.

Wall Street is still giving Apple time on AI

Apple’s stock rally continued even though the company still hasn’t fully released several major Apple Intelligence upgrades it previewed earlier in 2026. The delayed features include the more personalized Siri experience Apple demonstrated during its AI rollout.

Google, Microsoft, OpenAI, and Samsung continued rapidly expanding their generative AI products throughout 2026. That pace increased pressure on Apple to prove it can stay competitive in AI without loosening control over its ecosystem.

Apple’s hardware revenue remains cyclical, while Services growth has become a more stabilizing force for investors.

Apple’s hardware revenue remains cyclical, while Services growth has become a more stabilizing force for investors.Wall Street appears increasingly willing to overlook Apple’s delayed AI rollout because the company’s core business continues generating enormous profit and cash flow. Many investors view Apple Intelligence as a long-term ecosystem and hardware-retention strategy, not an immediate revenue engine, tied to future iPhone, iPad, and Mac upgrades.

WWDC 2026 is now becoming the next major catalyst for Apple shares. Analysts expect Apple to preview additional Apple Intelligence features, expanded developer tools, and a more capable Siri system during the conference, which begins June 8.

Several Wall Street firms have described WWDC 2026 as a critical test for Apple’s AI strategy after months of criticism that the company moved too slowly following the generative AI boom.

Apple’s rally suggests investors still believe the company can afford to move slower on AI than many rivals.

Apple’s scale continues insulating the company

Apple’s latest rally also reflects how differently investors treat the company compared to smaller technology firms chasing AI growth.

Many companies tied to AI infrastructure or software saw enormous valuation increases during 2025 based largely on future growth expectations. Apple, by contrast, already operates at a scale where investors prioritize stability, margins, ecosystem retention, and long-term cash generation over rapid expansion.

The company continues generating more revenue and profit than most consumer technology companies. Those financial results give investors confidence that Apple can withstand setbacks more easily than many rivals.

Apple recovered even as investors continued questioning the pace of its AI rollout, future regulatory pressure, and long-term iPhone growth. The stock’s record close above $300 shows Wall Street still values Apple’s core business strength more than near-term concerns about Apple Intelligence.

Stephan is the sports journalist for the Maple Grove Report.